Distilling Frenzy #6: Capitalism is Communism, Against Indefinite Attitudes

Welcome to this issue of Distilling Frenzy. Musings on our Paleolithic emotions, medieval institutions, and God-like technologies. Often derivative, sometimes insightful. Frequency irregular. For selection of past essays, click here.

This past week has seen news of a hopeful COVID-19 vaccine. I would like to use this piece of news as a launchpad to depart from the usual programming to explore interesting tensions in financial capitalism and modernity more generally. As always, feedback welcome.

Capitalism is Communism

The horseshoe theory of ideology posits that the far-left and the far-right, rather than being at opposite and opposing ends of a linear political continuum, closely resemble one another, analogous to the way that the opposite ends of a horseshoe are close together.

Similarly, there is a sense in which capitalism and communism have converged. Consider the coronavirus: COVID-19 has obviously been bad for the economy and COVID-19 vaccines would obviously be good for the economy.[1] Econ 101 suggests that the solution would be for companies to turn a profit by making COVID-19 vaccines and selling them at a price exceeding costs.

The previous sentence obscures a great deal of complexity. Reasonable people can and do disagree on the ideal ways of funding, producing and distributing pharmaceutical products. A big part of the problem is making money through life-saving vaccines is a bad look.[2]

Fortunately, shareholder capitalism, coupled with the rise in passive investing, promises to save the day. In 2019, index funds that passively invest in stocks have exceeded active funds for the first time in the US.

As a result, there are basically a handful of institutional investment firms whose jobs are to hold onto a diversified portfolio of stocks that represent “the market”. (Here is an interesting side note on power law distributions in passive investing.) This portfolio of stocks includes huge, publicly traded pharmaceutical companies like Pfizer Inc.

If Pfizer is the first to market, there is a great asymmetry in the potential upsides to these passive funds as shareholders of Pfizer vs as shareholders of stocks representing “the market” generally. As Matt Levine writes:

BlackRock, for instance, owns about $16 billion of Pfizer stock. If Pfizer went to zero—if it bankrupted itself, selflessly producing and distributing vaccines—BlackRock (really its clients) would lose $16 billion. BlackRock owns about $2.9 trillion of other stocks; if a coronavirus vaccine allowed businesses to reopen and normal economic life to resume, and as a result those other stocks went up by 1 percent, that would more than make up for bankrupting Pfizer.

As such, government interventions to nationalize drug companies or impose price caps or suspend patent laws are unnecessary. Pfizer’s own large diversified shareholders are already incentivized to ensure COVID-19 vaccines are distributed in a way to ensure the economy experiences a broad recovery.

This is thematically resonant with my earlier essay on the distinction between value creation and value capture. Here, COVID-19 vaccines would obviously create far greater value than can be captured by pharmaceutical companies. (Indeed, the canonical way to bet on COVID-19 vaccines is not Pfizer’s stocks, but airline and cruise stocks.) Returning to Econ 101, these positive externalities imply that the merely self-interested Big Pharma will devote insufficient resources to such activities.[3]

However, thanks to the rise of passive investing, institutional investment firms like BlackRock are well-placed to “internalize the externality” and play a state-like role in solving this coordination problem. As Levine points out, such “externality internalization” has been manifested in other ways, such as BlackRock’s steps towards directing capital away from companies that “present a high sustainability-related risk”, motivated by climate change concerns.

Of course, the eagle-eyed reader will readily poke holes in this story.

For one, there is no evidence that large institutional investors like BlackRock have done anything remotely similar to bankrupting Pfizer to save the world, nor do they have reason to. The whole point of passive investing is to be, well, passive. Furthermore, in other contexts, the pursuit of these investors’ interests—whether via explicit coordination or implicit understanding—raises antitrust concerns: plausibly, if the major companies in a given industry are all owned by the Big Three index-fund companies, managers seeking to maximize value for their actual shareholders should collude rather than compete. (There is no clear evidence that this has happened.)

Another objection is that the world-saving company in question might not be within the warm embrace of passive index funds. As Levine himself noted, out of the drug companies contending to produce COVID-19 vaccines (as of July 2020, anyway), “Moderna has more concentrated owners than the bigger companies” and “[i]f you don’t like drug profits maybe you have to regulate them or nationalize them or whatever, that’s not my problem, that’s Congress’s problem.”

I’m sorry I lied. Capitalism is not communism, after all.

Against Indefinite Attitudes

A core insight in Taleb’s Antifragile is that there is an inverse relationship between the fragility of a system and the fragility of its components. The quality and reliability of local restaurants as a collective are owed to the fragility individual restaurants. The financial system is brittle because banks are too big to fail. The DMV is notoriously inefficient because you can’t get rid of civil servants. So on and so forth.

By the same logic, a healthy economy must have a certain turnover of startups that go on to replace established companies. Whereas other sectors of finance facilitate this turnover (venture capital, private equity or just active investing in general), passive investing is a bet that the future largely belongs to large, incumbent companies.

It is now conventional wisdom that passive investing will generally outperform active investing after accounting for the cost. However, a la Kantian ethics, passive investing is not universalizable and necessarily free-rides on the efforts of active investors. This has led to the criticism that passive investing is worse than Marxism. The latter at least contends that the state has a defeasible view on how resources should be allocated. In contrast, the former is an abdication of responsibility.

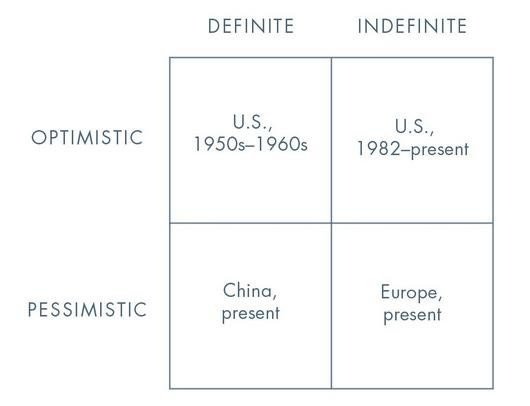

We can generalize this further beyond a mere asset allocation problem. In Peter Thiel’s cult classic Zero to One, he draws a sharp distinction between definite and indefinite attitudes using the following 2x2 matrix:

Peter Thiel writes:

Indefinite attitudes to the future explain what’s most dysfunctional in our world today. Process trumps substance: when people lack concrete plans to carry out, they use formal rules to assemble a portfolio of various options. This describes Americans today. In middle school, we’re encouraged to start hoarding “extracurricular activities.” In high school, ambitious students compete even harder to appear omnicompetent. By the time a student gets to college, he’s spent a decade curating a bewilderingly diverse résumé to prepare for a completely unknowable future. Come what may, he’s ready—for nothing in particular.

A definite view, by contrast, favors firm convictions. Instead of pursuing many-sided mediocrity and calling it “well-roundedness,” a definite person determines the one best thing to do and then does it. Instead of working tirelessly to make herself indistinguishable, she strives to be great at something substantive—to be a monopoly of one. This is not what young people do today, because everyone around them has long since lost faith in a definite world. No one gets into Stanford by excelling at just one thing, unless that thing happens to involve throwing or catching a leather ball.

There is much to quibble about both the framework and the specific examples. Nonetheless, Thiel’s distinction drives at something fundamental about modernity.

In the face of endless possibilities and dizzying complexity, the conventional wisdom is to adopt an attitude of indefinite optimism: to accumulate options and to avoid concentrated risks.

We see this in practice. People are marrying and having children later because there is always someone else to swipe right on Tinder. Bright students flock to prestigious colleges and then to versatile career paths like investment banking and consulting thereafter. Geographic mobility in the US is at historically low levels. Passive investing’s victory over active investing is but indefinite optimism’s latest triumph over definite optimism.

Yet, the world is shaped by risk-takers with a definite view of the future.[4] The aforementioned COVID-19 vaccine is really the product of both Pfizer and BioNTech. The latter is a German biotech company founded by Turkish immigrants in 2008 “to develop technologies for individualized cancer immunotherapies”. One does not simply move to another country and start a company without definite optimism.[5]

I have come here to bury indefinite optimism, not to praise it. However, the problem with convention wisdom is that it is usually right. The prisoners’ dilemma is dicey precisely because it is the dominant strategy to defect. Similarly, awareness that indefinite optimists free-ride on their definite counterparts does not dissolve the conflict.

It would also be thoroughly irresponsible for me to urge my readers to make long-distance moves, start a company, or generally take huge, unhedged bets. Instead, I offer something less radical: add a twist of definiteness to your life.

For example, most retail investors would do well to adhere to index investing and not delude themselves into thinking that they are the next Warren Buffett. However, consider holding holding small but significant positions, whether it be TSLA, BTC, or your crazy uncle’s favorite penny stock. Doing so not only discharges one’s duty to definiteness, it also makes for good conversation fodder at parties. There is much more to life than wealth maximization, after all.

I leave it to the reader’s good sense to generalize this to other aspects of life.

[1] As an aside, with the benefit of hindsight, the perceived tradeoff between pandemic control and economy recovery—drummed up in no small part by the media that thrives on imbuing real-world events with Manichean themes and serving such content to the willing masses—has always been absurd.

[2] Indeed, Bill Gates himself said Covid-19 medication and future vaccines should be distributed to people who need them the most and not to the highest bidder. (However, according to social-desirability bias, the most illuminating and underrated bias, in my opinion, you would expect one of the World’s Richest Persons™ to say exactly that.)

[3] In fairness, this nerdy focus on “positive externality” and “value capture” is somewhat myopic, especially in light of the themes of that previous essay. After all, there is a good case to be made that civilization is basically built upon positive externalities created by those who came before us.

In parallel, it is retrospectively clear that there is a set of government actions that, if taken, would have avoided much of the value destruction wrought by COVID-19 and different governments have managed to converge upon that set of actions to differing extent. Alas, contrary to the current discussion on private actors, it is much harder to have that discussion in a similarly objective fashion.

[4] It must be noted that this includes both the risk-takers who succeeded and those who failed. Failure is often valuable source of information that can only be obtained inductively, information that helps the risk-taker who eventually succeed, to the benefit of us all. Alas, the podium is noisy and the graveyard is silent.

Consider Taleb’s idea of a National Entrepreneur Day, with the following message: “Most of you will fail, disrespected, impoverished, but we are grateful for the risks you are taking and the sacrifices you are making for the sake of the economic growth of the planet and pulling others out of poverty. You are at the source of our antifragility. Our nation thanks you.”

For a dramatic example of definite optimism, even by Silicon Valley standards, read this.

[5] This speaks to my central unease living in Singapore. Like the US, Singapore is an immigrant society built by forefathers who took a chance and moved to a foreign land. Yet, today, the same indefinite attitudes pervade Singapore. The political leadership is drawn almost exclusively from the public sector and the risk-free, protected-by-regulations parts of the private sector (legal and medical professionals, mostly). The economy thrives on secondary services that are founded on risk-taking by people in other parts of the world. Poignantly, the list of richest Singaporeans is topped by a naturalized hotpot restauranteur from China.

It is hard to be bearish on Singapore. Singapore’s key competitive advantages—a nimble political system, a regional legal and standard-of-living arbitrage, a well-educated workforce—are not going away anytime soon. Yet, there is a sense that the most important work has been done and Singaporeans are experiencing a Fukuyama-esque “end of history”, living off the economic rents produced by the hard work and risk-taking of an earlier generation.